Top Software License Management Options in 2026 and When to Choose Holograph

Key Takeaways

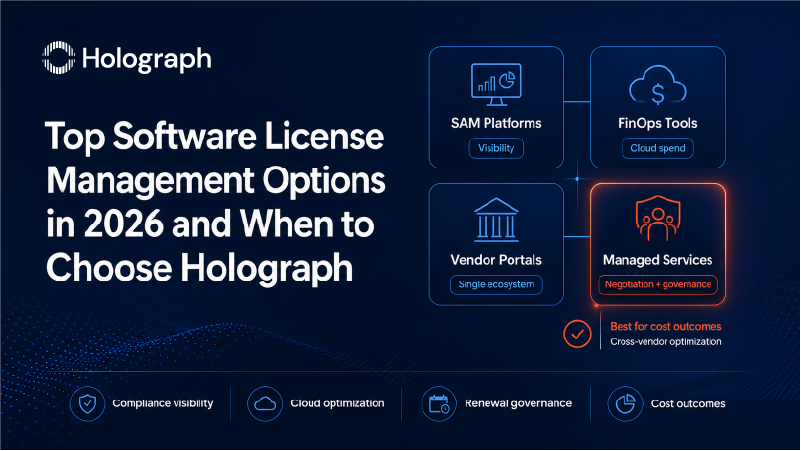

- The enterprise license management landscape in 2026 spans four distinct categories: SAM platforms, FinOps tools, vendor-specific management portals, and managed license services partners. Each category serves a different function, and most enterprises at scale need capabilities from more than one.

- Mordor Intelligence's 2025 ITAM market analysis reports that large enterprises account for 64.36% of SAM market share, with North America representing 38.20% of global revenue. The investment is substantial, but spending on tools does not automatically translate into license cost reduction.

- SAM platforms (Flexera, ServiceNow SAM) provide visibility and compliance. FinOps tools (CloudHealth, Kubecost, Spot.io) optimize cloud consumption. Vendor portals (AWS License Manager, Microsoft Admin Center) manage individual ecosystems. Managed services partners (Holograph) deliver cross-vendor negotiation, renewal governance, and measurable cost outcomes.

- The best software license management approach in 2026 depends on vendor count, spend threshold, internal expertise, and whether the goal is compliance visibility or actual cost reduction.

Introduction

Enterprises evaluating the best software license management options in 2026 face a market that has expanded considerably since the days when "license management" meant a spreadsheet and a renewal calendar. The landscape now includes dedicated SAM platforms, cloud-native FinOps tools, vendor-specific management portals, and managed services partners, each claiming to solve the license cost problem.

The challenge is that these categories overlap in marketing language but diverge significantly in practice. A SAM platform and a managed services partner both promise "license optimization," but one delivers a dashboard while the other delivers negotiated savings. A FinOps tool and an SAM platform both claim "cost visibility," but one tracks cloud resource utilization while the other reconciles software entitlements.

Mordor Intelligence's 2025 IT Asset Management market report puts the scale of this investment in context: large enterprises hold 64.36% of the SAM market share, and the fastest-growing segment (SMEs) is expanding at 17.59% CAGR. The money flowing into license management tools is real. The question for 2026 is whether that investment is reaching the right category for the organization's actual needs.

This guide walks through each category, identifies what each does well and where each falls short, and provides a decision framework for matching the right approach to the right enterprise situation.

Category 1: SAM Platforms

Key players: Flexera One, ServiceNow SAM, Certero for Enterprise SAM, USU SAM, Ivanti

SAM platforms are the most established category in software license management. They automate software discovery, reconcile installed software against purchased entitlements, and generate compliance reports for audit defense.

The category underwent significant consolidation in recent years. Flexera completed its acquisition of Snow Software in 2024, combining two of the largest SAM vendors into a single entity serving over 50,000 customers. Flexera subsequently acquired ProsperOps to strengthen its FinOps capabilities, signaling that even SAM platform vendors recognize the need to bridge the gap between license management and cloud cost optimization.

ServiceNow SAM has gained traction among enterprises already running ServiceNow for ITSM, offering the advantage of a unified platform for IT service management and asset management. Certero has earned strong marks for engineering-specific SAM, and USU continues to serve the European enterprise market.

Strengths

SAM platforms provide the deepest automated discovery capabilities. They scan networks, endpoints, servers, and cloud environments to identify installed software, then normalize the data into a single inventory. For large enterprises running thousands of applications, this automated inventory is the data foundation that every optimization effort requires.

Compliance reporting is the second core strength. When a vendor audit arrives, the SAM platform generates the entitlement-vs-deployment report that serves as the organization's primary defense. This capability alone justifies the investment for enterprises in audit-heavy industries.

Limitations

SAM platforms do not negotiate with vendors. They identify that 600 Adobe Creative Cloud licenses are deployed but only 380 are in active use. They do not contact Adobe to restructure the ETLA, negotiate a per-seat reduction, or coordinate the timing with the renewal window.

They also require significant internal expertise to operate effectively. Configuration, data normalization, and ongoing maintenance demand dedicated SAM analysts, and the time from deployment to actionable insights typically spans 6 to 12 months.

Best for: Enterprises with dedicated SAM teams, compliance-first priorities, and environments heavily weighted toward on-premises or traditional licensing.

Category 2: FinOps Platforms

Key players: CloudHealth (VMware), Kubecost (IBM), Spot.io (NetApp), Apptio Cloudability (IBM), nOps

FinOps platforms emerged from the cloud cost management space and focus specifically on optimizing infrastructure consumption in AWS, Azure, and Google Cloud. The category has undergone its own consolidation wave. IBM's acquisition of Kubecost in 2024 followed its earlier acquisitions of Apptio and Turbonomic, creating a combined platform that spans Kubernetes cost management, application performance, and FinOps across all major cloud providers.

CloudHealth, now part of VMware by Broadcom, remains one of the most widely deployed FinOps tools, typically priced at approximately 3% of monitored cloud spend. Spot.io (NetApp) specializes in real-time compute optimization, and nOps focuses on automated savings for AWS-heavy environments.

Strengths

FinOps platforms excel at real-time cloud cost visibility. They track resource utilization by the hour, identify oversized instances, flag idle resources, and recommend reserved instance purchases or savings plan commitments. For enterprises with $1 million or more in annual cloud infrastructure spend, these tools deliver measurable savings on the consumption side of the budget.

The cultural contribution is also significant. FinOps platforms enable cost allocation and showback models that create accountability across engineering and product teams, shifting cloud spending from an opaque IT expense to a visible, manageable cost center.

Limitations

FinOps platforms do not manage SaaS seat licenses, on-premises entitlements, or enterprise agreement terms. They optimize how much compute you consume, not how many Microsoft 365 seats you are paying for, what tier of Atlassian Cloud you are on, or when your Adobe ETLA renewal is approaching.

As we've detailed in our comparison of SAM, FinOps, and managed services, FinOps typically covers 30 to 40% of an enterprise's total software spend (the cloud infrastructure portion), leaving the remaining 60 to 70% in SaaS subscriptions and on-premises licenses untouched.

Best for: Cloud-heavy organizations with significant AWS, Azure, or GCP spend and established FinOps maturity.

Category 3: Vendor-Specific Management Tools

Key players: AWS License Manager, Microsoft 365 Admin Center, Adobe Admin Console, Atlassian Admin, Google Workspace Admin

Every major software vendor provides some form of license management portal. AWS License Manager tracks BYOL (Bring Your Own License) deployments and managed entitlements. Microsoft's Admin Center provides seat assignment and usage reporting for M365 and Azure. Adobe's Admin Console manages Creative Cloud and Document Cloud seat allocation. Atlassian Admin shows Cloud subscription details and user access.

Strengths

These tools are free, already available, and authoritative for their respective ecosystems. AWS License Manager is the most accurate source of truth for AWS license deployments. Microsoft Admin Center provides the definitive view of M365 seat assignments. No third-party tool will ever have more accurate data about a specific vendor's environment than the vendor's own management portal.

Limitations

The obvious constraint is scope. Each portal manages only its own ecosystem. The Microsoft Admin Center tells you nothing about your Atlassian spend. AWS License Manager provides no visibility into your Adobe ETLA. For an enterprise running five or more major vendors, checking each portal independently and attempting to reconcile the data manually recreates the spreadsheet problem that SAM tools were designed to solve.

More critically, vendor portals are designed to manage your relationship with that vendor, not to optimize your costs across vendors. The incentive structure is inherently one-directional: the portal helps you use more of the vendor's products, not less.

Best for: Small organizations with one or two primary vendors, or as a supplementary data source feeding into a SAM platform or managed services engagement.

Category 4: Managed License Services Partners

Key players: Holograph Technologies, Anglepoint, SoftwareOne/Crayon, Insight Enterprises

Managed license services represent the newest category in the best software license management landscape for 2026, though the model has existed in various forms for over a decade. The category earned formal analyst recognition when both Gartner and IDC published dedicated assessments of managed SAM services in 2025, establishing it as a distinct market alongside SAM tools.

The managed services model differs from the previous three categories in a fundamental way. The deliverable is outcomes, not software. A managed services partner conducts the license assessment, identifies optimization opportunities, negotiates with vendors, implements changes, and monitors the environment on an ongoing basis. The enterprise's internal team does not need to build SAM expertise or operate additional tools.

Strengths

Negotiation capability. This is the single largest differentiator. No SAM platform, FinOps tool, or vendor portal negotiates with software vendors on the enterprise's behalf. A managed services partner leverages market knowledge, multi-client benchmarking data, and established vendor relationships to negotiate renewal terms, true-downs, tier restructuring, and co-termination agreements. This negotiation layer is where the largest cost recoveries materialize.

Cross-vendor optimization. Partners managing portfolios across Atlassian, Microsoft, Adobe, AWS, Google, and GitLab can identify optimization opportunities that single-vendor tools miss entirely. Holograph's multi-OEM partnership model spans all six of these ecosystems, enabling the cross-portfolio perspective that produces compound savings.

Speed to value. Where SAM platforms require 6 to 12 months for deployment and data normalization, a managed services engagement typically delivers its first optimization recommendations within 30 to 60 days and implements negotiated savings within the first quarter. Holograph has documented 40% cost savings for enterprise clients through this model, a result that reflects both the negotiation leverage and the cross-vendor optimization that tools alone cannot provide.

Limitations

Managed services require trust in an external partner. The organization is sharing license data, vendor contract details, and spending information with a third party. Partner selection matters. For enterprises evaluating the best software license management options in 2026, the evaluation should include vendor relationships, industry experience, client references, and the partner's track record of quantified outcomes rather than generic consulting promises.

Best for: Multi-vendor enterprises with $2 million or more in annual license spend, organizations facing audit pressure across multiple vendors, and teams that lack the internal resources to build and maintain a dedicated SAM practice.

Decision Matrix: Matching Your Situation to the Best Software License Management Approach in 2026

| If your situation is... | Start with... | Add later... |

|---|---|---|

| Single cloud provider, FinOps-mature team | FinOps platform | SAM platform when SaaS/on-prem grows |

| 1–2 vendors, strong internal SAM team | SAM platform + vendor portals | Managed services for renewal negotiations |

| 3–5 vendors, $1–3M license spend | SAM platform + managed services partner | FinOps platform for cloud layer |

| 5+ vendors, $3M+ license spend, audit risk | Managed services partner as primary | SAM platform as data layer, FinOps for cloud |

| Limited internal IT/SAM resources | Managed services partner | Vendor portals for day-to-day administration |

The enterprises that capture the full optimization opportunity described in our comprehensive licensing guide are typically running a combination: SAM platform for automated discovery, FinOps for cloud cost management, and a managed services partner for negotiation and governance.

When Holograph Is the Right Choice

Holograph Technologies operates as a managed license services partner with multi-OEM relationships spanning Atlassian, Microsoft, Adobe, AWS, Google, and GitLab. The engagement model follows a structured process: discovery and assessment, optimization recommendations, vendor negotiation, implementation, and ongoing monitoring.

The profile of enterprises that benefit most from Holograph's model includes these characteristics: four or more major software vendors in the portfolio, annual license spend exceeding $2 million, renewal cycles consuming disproportionate procurement time, audit history or audit risk across multiple vendors, and an internal IT team that is stretched too thin to dedicate resources to license governance.

Holograph's track record includes 170+ enterprise engagements worldwide, documented results including 40% cost savings and 60% faster performance outcomes, and delivery capability across three global offices (United States, India, and Saudi Arabia).

For enterprises already running SAM tools and wondering why costs have not decreased, the answer is often that the data layer is working but the execution layer is missing. Our detailed comparison of Holograph vs. SAM tools explores this gap in depth.

Next Steps

The best software license management strategy in 2026 is not a single tool or a single partner. It is a combination tailored to the enterprise's vendor landscape, spend profile, internal capabilities, and strategic priorities.

For enterprises ready to evaluate whether a managed services partner should be part of that combination, Holograph offers a complimentary license optimization assessment. The assessment covers the full multi-vendor portfolio and produces specific, quantified recommendations, not a generic capabilities overview.

Primary CTA: Request a License Optimization Assessment → Secondary CTA: Download the Almajdouie Case Study → — See how a logistics enterprise achieved 40% cost savings through Holograph's managed license services.

Related Reading

- Software License Management vs SAM vs FinOps: Choosing the Right Approach (MOFU-UC-3 comparison)

- Holograph vs Traditional SAM Tools: When a Services Partner Beats a Tool-Only Approach (BOFU-COMP-1 detailed comparison)

- How a Saudi Logistics Enterprise Cut License and Service Costs by 40% (Case study)

- How an Automotive Parts Leader Achieved 60% Faster Performance with Atlassian (Case study)

- Software Licensing Management and Cost Optimization Services (Service page)

This blog is part of Holograph's Software Licensing Management content series. For a deep dive into how Holograph compares to traditional SAM tools, read our detailed comparison. For the complete guide to enterprise license management, start with the pillar page.